When Alphabet announced a proposed US$80 billion equity capital raise to fund its expanding AI infrastructure, the immediate reactionwas surprise. After all, this is one of the most profitable companies in history. Alphabet generates more than US$170 billion in annual operating cashflow, holds one of the strongest balance sheets in corporate America, and has virtually unlimited access to global debt markets.

So why raise equity?

For large publicly listed companies in the US, equity is typically viewed as the most expensive form of capital. Issuing new sharesdilutes existing shareholders, while debt is generally considered a lower-cost source of funding. It's one of the reasons mature public companies tend tofavour debt over follow-on equity raises whenever possible.

That makes the proposal particularly interesting. Despite having one of the strongest balance sheets in the world, Alphabet chose toissue equity rather than continue funding its AI infrastructure expansion entirely through debt.

The decision demonstrates an important principle that applies to businesses of every size: the cheapest source of capital is not fixed. It changes as a company evolves.

The proposed transaction offers a valuable case study in capital allocation, particularly for founders and CFOs thinking about how to balance cash flow, debt and equity as their businesses grow.

How businesses typically finance growth

Regardless of whether a business is raising $5 million or $80 billion, there are broadly three ways to finance investment.

- Internally generated cash flow: This is typically the cheapest form of capital because it carries neither interest nor dilution. Profitable businesses can reinvest earnings directly into growth, making retained cash the preferred funding source wherever possible.

- Debt: Borrowing allows companies to accelerate growth while preserving shareholder ownership. For businesses with predictable revenue and sufficient cash flow to service repayments, debt often provides alower cost of capital than issuing additional equity.

- Equity: By issuing new shares, companies access permanent capital without creating repayment obligations. The trade-off is dilution, as existing shareholders own a smaller percentage of the business. For this reason, equity is often perceived as the most expensive funding option.

In reality, however, these three sources of capital are not static alternatives. Their relative attractiveness changes depending on a company's profitability, leverage, valuation and future funding requirements.

Why operating cash flow wasn't enough

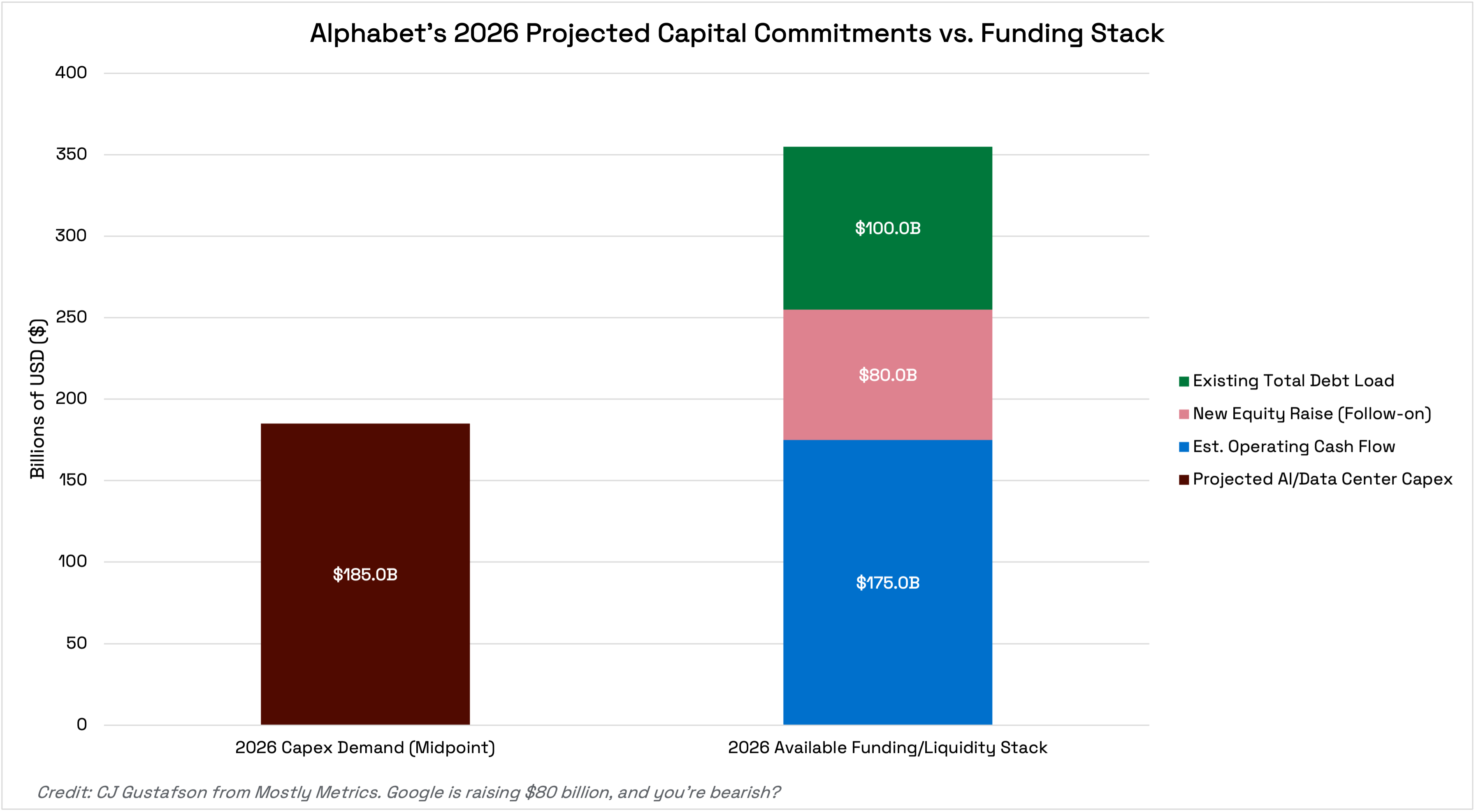

Alphabet's cash generation is extraordinary. Over the past twelve months, the business generated approximately US$174 billion in operating cash flow.

Under normal circumstances, this would comfortably fund most investment programmes. AI infrastructure, however, is anything but normal.

The company expects capital expenditure of between US$180 billion and US$190 billion during 2026, with spending forecast to increase again in 2027. Building hyper scale data centres, expanding global compute capacity and purchasing advanced AI hardware requires investment on a scale rarely seen in corporate history.

Despite generating enormous amounts of cash, Alphabet's investment requirements now exceed what operating cash flow alone can support.

That naturally leads to the second source of capital.

Why Alphabet didn't simply borrow more

Alphabet has already demonstrated a willingness to utilise debt markets. Over the previous year, the company issued more than US$85 billion of debt across multiple currencies, increasing total borrowings substantially.

For many businesses, the obvious next step would simply be to continue borrowing.

However, as debt levels increase, so does financial leverage. Higher leverage can increase borrowing costs, place pressure on credit ratings and reduce financial flexibility for future investment opportunities. Every additional dollar of debt becomes incrementally more expensive than the last.

Eventually, there comes a point where issuing another dollar of debt costs more than issuing another dollar of equity.

That appears to be the conclusion Alphabet reached.

When equity becomes the cheaper source of capital

The cost of capital isn't static. It changes as a company's valuation, leverage and financing options evolve.

At a market capitalisation of almost US$4 trillion, Alphabet's shares have become an exceptionally efficient funding currency. Issuing less than 2% additional equity allows the company to raise approximately US$80 billion while only modestly diluting existing shareholders.

At the same time, the economics of debt have changed. After issuing more than US$85 billion of debt over the previous year, every additional dollar borrowed would likely come at a higher marginal cost. Continuing to fund AI infrastructure entirely through debt would increase leverage, place greater pressure on Alphabet's balance sheet and ultimately raise its weighted average cost of capital (WACC).

Rather than continue pulling on the debt lever, Alphabet chose to rebalance its capital structure.

In simple terms, it recognised that its equity had become its most efficient source of capital.

That's a subtle but important shift in thinking. Rather than asking whether debt or equity is "better", Alphabet asked which source of capital created the lowest overall cost of funding for the next phase of growth.

Matching capital to the asset

Alphabet is investing in physical infrastructure that is expected to underpin its AI strategy for decades. While individual chips will eventually be replaced, the data centres, land, power infrastructure and networks represent long-term strategic assets.

Long-term infrastructure is generally best funded with long-term capital.

Using equity to fund infrastructure with a multi-decade lifespan creates a more permanent capital base than relying exclusively on additional debt. It also reduces refinancing risk and preserves borrowing capacity for future opportunities.

Executing an equity raise matters as much as deciding to do one

A transaction of this size has the potential to put significant pressure on a company's share price if new shares are simply issued into the market. Alphabet instead proposed a combination of a traditional public offering, an at-the-market (ATM) program, convertible preferred securities and a private placement to Berkshire Hathaway. Together, these structures are designed to broaden the investor base, create a more predictable dilution profile and reduce disruption to the market.

The lesson extends beyond public markets. Whether raising equity from existing investors, new investors or the public market, the quality of execution matters. A well-structured capital raise doesn't just minimise the cost of capital, it helps preserve confidence among shareholders and other stakeholders.

Why this matters for private companies

Very few companies will ever contemplate an $80 billion capital raise, but the principle is highly relevant for private businesses.

Companies often think about funding as a choice between debtor equity. In reality, both should be viewed as tools within a broader capital strategy. The right mix depends on factors such as valuation, cash generation, borrowing capacity and the purpose of the capital being raised.

That's exactly why many later-stage technology companies introduce venture debt alongside equity, rather than viewing the two as mutually exclusive.

A company with a strong valuation may choose to issue a smaller amount of equity while preserving debt capacity for future acquisitions or working capital.

Another business with predictable recurring revenue may find venture debt materially lowers its overall cost of capital while extending runway between equity rounds.

Lessons for founders and CFOs

- Capital structure should evolve alongside yourbusiness. Every business should view cash flow, debt and equity ascomplementary funding tools rather than competing alternatives.

- The cheapest source of capital changes overtime. As valuations increase, equity may become a more attractive source of capital. As cash flows become more predictable and borrowing capacity expands, debt may become increasingly attractive. Effective capital allocation requires continuously reassessing these trade-offs rather than relying on fixed assumptions.

- Match your funding to the asset you're financing. If management is making a long-term investment that will shape the business for decades, the capital structure should reflect that same long-term horizon.

Every funding decision is ultimately a capital allocation decision.

The businesses that create the most long-term shareholder value aren't those that always choose debt or always choose equity. They're the ones that understand when to use each.

Google may be operating at a different scale, but the principle is exactly the same for a Series A startup, a late-stage private company or an ASX-listed business.

Sources:

Alphabet investor announcement, CNBC and Reuters reporting, and analysis inspired by CJ Gustafson's Mostly Metrics newsletter.